Imagine this: you’re in front of a nervous young entrepreneur pitching their idea for the next Uber. They are a first time entrepreneur whom you met at a cocktail networking event, an event you didn’t even want to attend. They are trying to convince you that their $10 million dollar valuation is warranted. Yet, they have no idea what a cap table is and no idea how they are going to monetize their business. You are so tired of asking the questions they should have already answered.

And then you ask yourself: how did I get here? Why did I even agree to take this meeting?

Sound familiar?

You might need to take the same advice that you’ve given to your entrepreneurs: take some time and figure out what your specialty is and what you want to focus on. For VCs, this implicitly defines your investment thesis.

As most of you already know, an investment thesis is the formula of beliefs and criteria used to determine what investments to pursue and why.

What We Look For

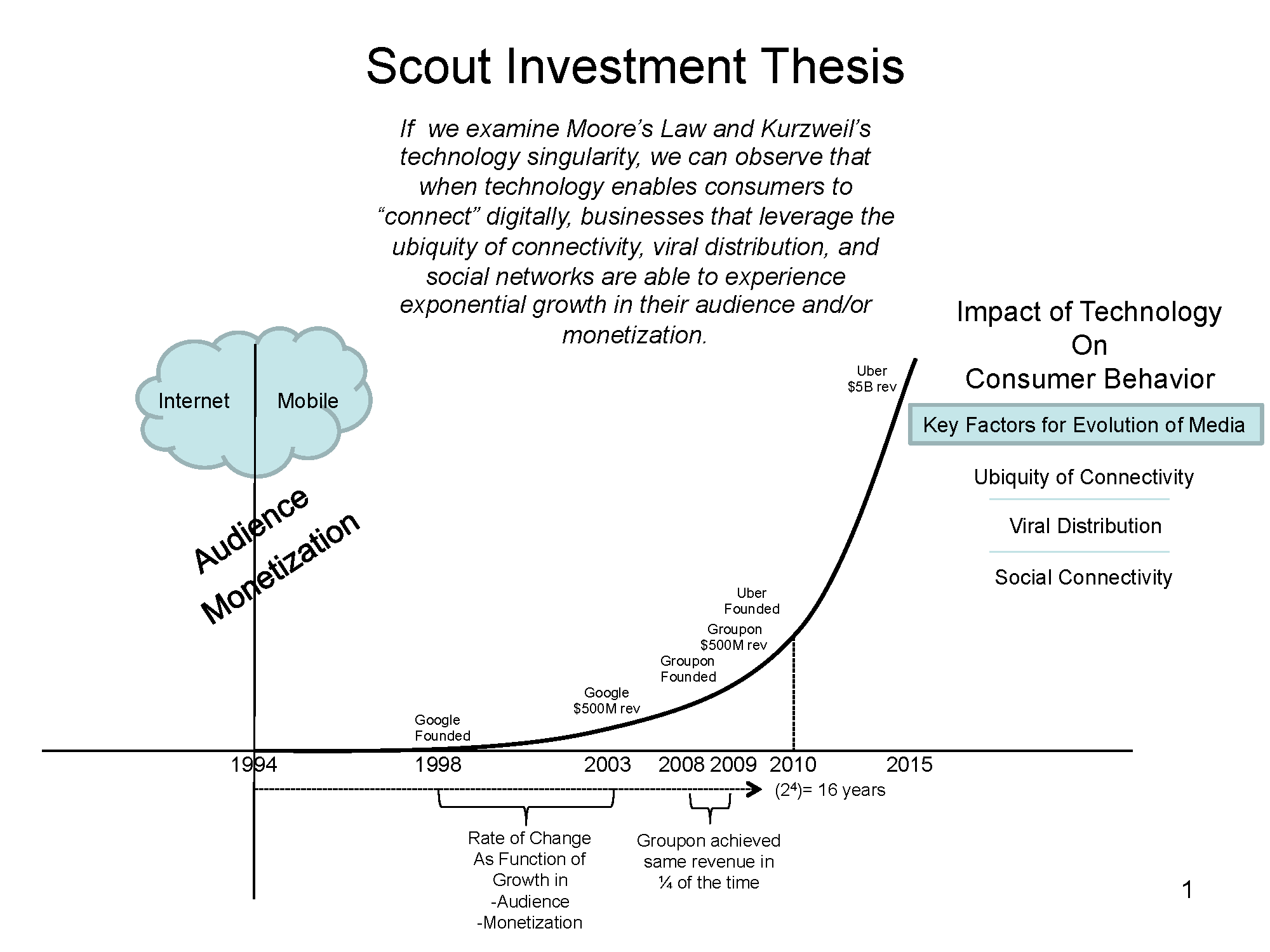

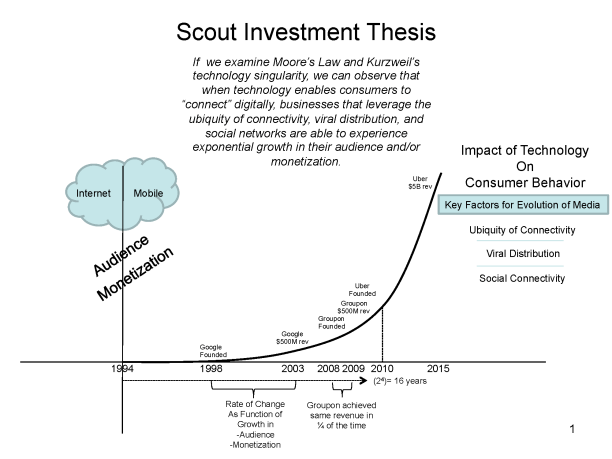

From the very beginning of Scout Ventures, we’ve put heavy importance on figuring out who we were as individuals and who we wanted to be as a firm. As the Founder, I knew I wanted to build a firm that explored how technology enables consumers to connect “digitally” and then leverage the ubiquity of connectivity, viral distribution and social networks to experience exponential growth in their audience and/or monetization.

Putting it in Practice

In order to explore and leverage these ideas, I knew we had to:

1) Put a process in place that would lead us to discover and invest in the best entrepreneurs and companies that fit with our own backgrounds and expertise, and

2) Figure out the best way we as a firm could then help these entrepreneurs and companies to evolve and grow into their potential.

Let’s talk about the process first. Over the past few years, we have established what we call ‘filters’. We refer to these when deciding to take a meeting and when we are considering investing. It is important to apply consistent filters across the board; for example, we know we don’t invest in HR based companies, so we would politely decline a meeting with one. Be sure to keep a growing list of filters to refer back to.

At Scout, we’ve identified over forty parameters that we use to evaluate a deal. These parameters range from highly quantitative statistics such as MRR and burn to more qualitative aspects such as founder balance and market structure dynamics. Through introspective analysis and reviewing our 55 investments, we have been able to develop pattern recognition techniques that identify what specific characteristics exist across our most successful portfolio companies.

If you are not established enough as an investor to be able to decide these from your own historical data, then start with qualitative filters. For example, we prefer to invest in seasoned entrepreneurs and in teams who we were introduced to via a trusted advisor, entrepreneur or friend. Through the use of simple filters and parameters we make sure we don’t take on too much, don’t take on anything where we do not feel we can add value and most importantly, we make sure stay true to our investment thesis.

If you are a new firm, don’t stress over this too much. It has taken years to truly establish our current base criteria for taking a call or listening to a pitch and deciding to invest. And don’t forget, your thesis and filters are also something that should be constantly evolving.

Investing More Than Money

I like to think that most VCs don’t just stop at finding the entrepreneur and writing a check. But that’s not always the case. Ever since I started investing years ago, I always found the most rewarding part to be what happens after the check has been written, and I’m not just talking about the potential monetary returns.

One of Scout’s key activities is adding value to those we invest in. We don’t just invest money; we invest time. We start helping the entrepreneur from the minute they walk into our office. When we feel that immediate connection and know that the chemistry works between our team and the entrepreneur(s), we’re already at work thinking about what we can do to help. The first thing we’ll do is open our rolodex and introduce them to people we know can help them in ways we might not be able to.

At Scout, we are entrepreneurs. Our venture just happens to be a venture capital firm. Because of this, we know first hand what struggles entrepreneurs are going through and will go through. And when we help you, we are not only taking into consideration our own experience building the firm, but also taking trends from the data we’ve collected on our 50+ investments. We’ve seen it all.

In summary, if you think your firm needs a thesis overhaul, or even the creation of a thesis, be sure to base it on what your team is passionate about but also on what is practical for the size of your firm and fund. After all, this is how you differentiate yourself from the ever increasing number of firms. The entrepreneurs you attract and invest in will mirror the quality and authenticity of your thesis, so don’t rush it.